Report Documents Economic Peaks and Troughs

|

NEW YORK — A recent report from the American Institute of Architects, designed to provide a market snapshot, paints a rosy portrait for architects prior to the economic downturn while offering a warning for firms in the market today.

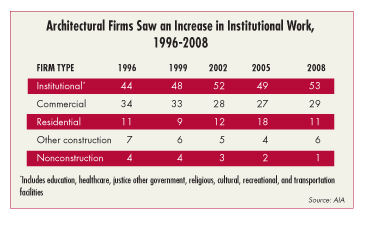

Institutional construction, which includes K-12 and higher education facilities, reached a 15-year peak before the recession in 2008, according to survey responses from 2,699 AIA-member firms that were collected between January and March of this year. However, firms in all market sectors have witnessed steep declines this year, according to the survey.

“At the time of this report, the full extent of the downturn from the recession is unknown, but it is clear that it will be substantial,” the report states. “Payroll figures, which are available from the U.S. Department of Labor for a wide range of industries, already point to major downsizing at many businesses.”

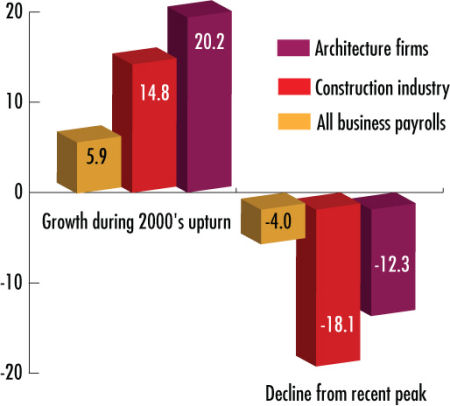

The report states construction companies experienced an 18 percent decrease in payrolls since residential construction peaked in 2006. Architectural firms, which avoided a decline until 2008, have experienced a 12 percent payroll reduction.

The report predicts the residential market will be first to experience a recovery, followed nonresidential projects. The most severely affected sector will be the commercial market, according to the report.

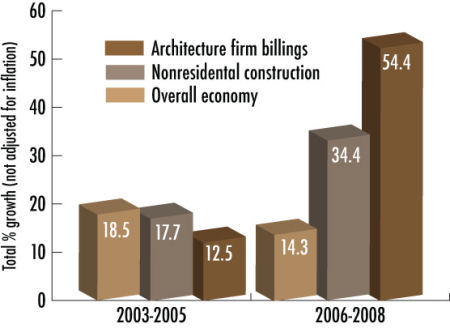

The current state of the market lies in contrast to earlier in the decade, when billings at U.S. firms increased $16 billion from 2005 to 2008, when they totaled $44.3 billion. During that time, gross architectural billings for nonresidential construction rose more than 50 percent and net billings rose more than 40 percent.

“While architecture firms are struggling considerably as the current economic slump continues unabated, there were extensive increases in revenue for the profession during the period this survey covered,” says Kermit Baker, AIA chief economist. “Of particular note, the survey also revealed the number of firms practicing green design has nearly doubled since 2005. The use of BIM software has also doubled in the last three years.”

Business Landscape

|

Despite recent mergers, architectural firms remain fragmented with 10 or less employees at almost 80 percent of AIA member-owned architectural firms at the end of last year. Only 2 percent of firms reported having 100 or more employees, according to the report.

However, despite the abundance of small firms, architectural firms with 50 or more employees generated half of the total revenue for all firms and employed 44 percent of the architectural workforce.

The AIA predicts that following extensive downsizing in 2008 and 2009, many architects will create smaller practices. Another effect of downsizing is the loss of interns or other young staff members who could leave the field for other career opportunities if they have difficulties finding work, according to the report.

During the recovery process after previous recessions, firms found a shortage of experienced staff as many people left architecture for other careers.

Additional highlights from the report:

- 50 percent of architecture firms reported green design practices, up from 31 percent in 2005. Firms with 10 to 49 employees had the biggest increase in green design with a jump from 48 percent to 72 percent in the last three years.

- The number of minority licensed architects increased from 11 percent to 18 percent from 2005. There was a 3 percent increase in the number of minority partners/principles. The number of women principles/partners and architectural staff increase 1 percent.

- The number of firms using BIM software increased from 34 percent in 2005 to 69 percent.

s s |

Top 10 Sectors Served by Architects in 2008

- Healthcare – 18.2%

- Office space – 11.3%

- Education (K-12) – 9.0%

- Education (college/university) – 9.0%

- Retail, food services – 8.4%

- Government/civic – 5.9%

- Hospitality – 4.8%

- Industrial – 3.6%

- Transportation – 2.9%

- Recreational – 2.3%